Beyond the Waiting Game: How AI Tracks and Neutralizes Hidden HOA Landmines Before Closing

Ask any senior title processor about their worst closing day horror stories, and there’s a good chance an HOA is the main villain. Everything else on the file can be spotless: the title search is clean, the lender’s wire is queued, and the borrower is ready to sign their closing package. Then, twenty-four hours before funding, an unexpected surprise surfaces. An unrecorded architectural violation, a delinquent special assessment, or a ghost management company that refuses to return calls suddenly brings the entire transaction to a screeching halt.

In title and settlement operations, Homeowners Association (HOA) data is notoriously unpredictable. It remains one of the few stages where closing teams feel entirely at the mercy of third parties who operate on their own timelines. When an estoppel letter gets stuck in limbo, it isn’t just an administrative headache. It puts the lender’s interest rate lock at risk, burns out your escrow staff, and threatens client trust right before the finish line.

The Real Friction Behind HOA Estoppels

Why do HOAs create such disproportionate chaos in the closing workflow? The bottleneck is rarely just a slow clerk or a delayed mail delivery. It stems from structural inefficiencies across community management systems.

A recent industry article, 7 HOA Problems That Delay Closings (And How to Solve Them), outlines the specific operational landmines title teams face every week:

- Ghost Contacts and Outdated Portals: Management companies merge or hand off accounts without updating public records, forcing processors to play phone tag with disconnected numbers.

- Surprise Processing Fees: Estoppel fees vary wildly across jurisdictions, and many management groups demand upfront, non-refundable rush fees before opening a file.

- Unrecorded Violations and Delinquent Dues: Outstanding fines for unapproved alterations or unpaid dues often go unmentioned until the formal certificate arrives—leaving no time to resolve disputes before closing.

- Incomplete Documents: Some HOAs provide certificates that miss required statutory data or carry aggressive expiration dates that force expensive last-minute re-orders.

When teams rely on spreadsheets and manual phone calls to manage these variables, small oversights quickly turn into high-stakes fire drills.

The High Cost of the “Search and Hope” Model

For years, the standard approach to managing HOA estoppels has been simple persistence: assign a processor to call, email, and follow up repeatedly until a document appears. But in a modern closing environment, this brute-force method breaks down fast.

When processors spend hours playing detective just to locate a dormant management company or track down a $50 fee discrepancy, they aren’t working on complex curative issues or serving clients. They are acting as expensive administrative switchboards. Worse, because manual follow-ups happen reactively, critical delays are discovered late in the cycle. By the time a team realizes an HOA has gone silent, the buyer’s rate lock is expiring and everyone is scrambling to salvage the transaction.

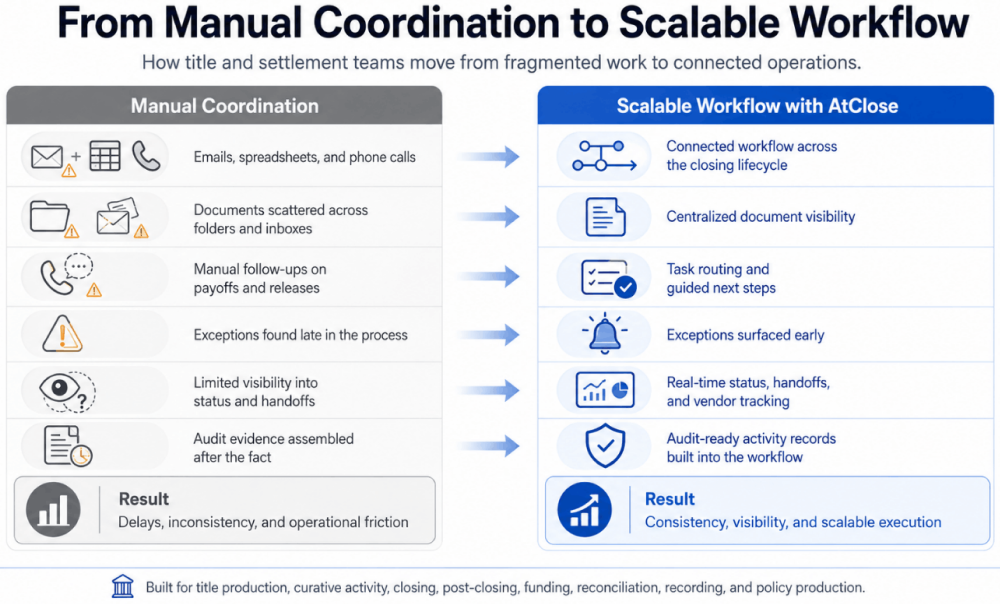

Moving from Reactive Chasing to Proactive Validation

Fixing the HOA problem requires moving past static task lists and reactive email checking. Modern settlement teams are replacing manual lookup loops with intelligent document processing and automated workflow engines—the core capabilities powering platforms like AtClose to transform chaotic document intake into clean operational data.

Instead of treating estoppels as an unpredictable waiting game, AI-driven automation builds proactive data validation directly into the order lifecycle:

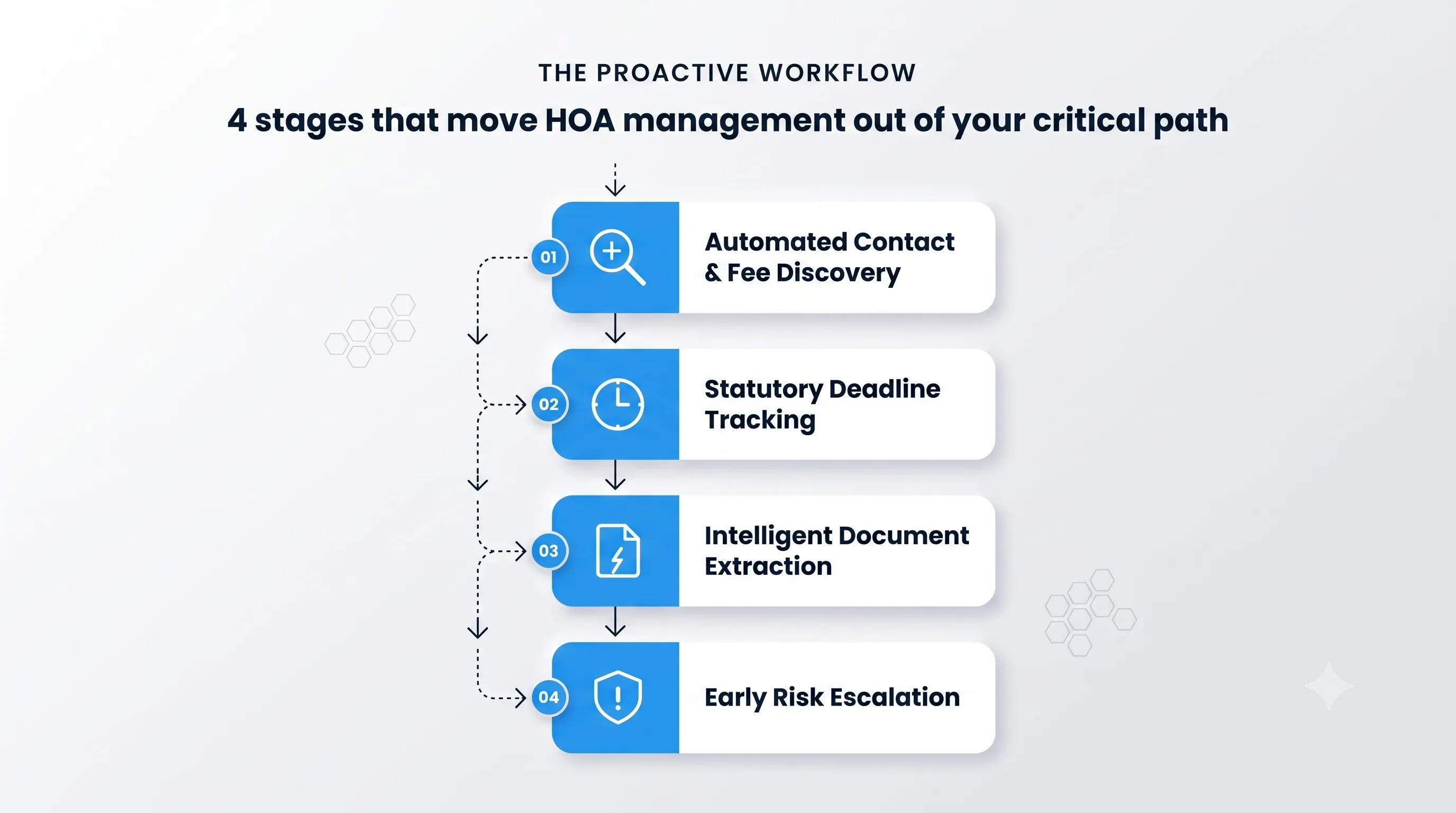

- Automated Contact and Fee Discovery: The system cross-references property addresses against verified databases, identifying correct contacts, required portals, and expected fee structures during order intake.

- Statutory Deadline Tracking: Instead of relying on manual reminders, the platform calculates statutory response windows based on state rules and issues automated follow-ups to management companies.

- Intelligent Document Extraction: The moment an estoppel certificate arrives, AI models analyze the document in seconds. The system extracts fee breakdowns, performs instant line-item reconciliation against expected figures, and flags unrecorded violations immediately.

Early Risk Escalation: If a management company misses a milestone or a document reveals a property violation, the system alerts the designated specialist right away. This gives your team days rather than hours to resolve the issue.

Protecting Margins and Relationships

Neutralizing HOA landmines isn’t just about avoiding last-minute stress; it directly drives operational profitability. By stripping out the manual friction surrounding HOA tracking, title agencies achieve higher file throughput without overloading their staff.

More importantly, proactive HOA management protects your reputation with key referral partners. Lenders and real estate agents notice when an agency consistently delivers smooth, on-time closings without eleventh-hour surprises. Eliminating uncertainty from third-party requests transforms your team from reactive paperwork processors into trusted strategic partners.

Clear the Path to the Closing Table

The hidden landmines in HOA estoppels don’t have to dictate your daily closing schedule or disrupt your operational margins. Combining intelligent document capture with automated workflow orchestration allows your team to catch exceptions early, protect lender timelines, and deliver a predictable settlement experience every single time.

Ready to take control of your closing pipeline and eliminate manual chasing? Explore how AtClose brings intelligent automation to your title operations today.